If you’re planning to claim 45Y, 45X, or 48E tax credits for solar projects beginning this year, you must comply with the new Foreign Entity of Concern (FEOC) restrictions established by the One Big Beautiful Bill Act (OBBBA). Projects or taxpayer entities not in compliance will not be eligible for any of the tax credits.

Find answers to common questions about the new FEOC rules for solar projects and manufacturers in this post, including information from the February 12 IRS guidance. If you like, you can read the full OBBBA here.

What are the new FEOC rules for solar developers and manufacturers?

For purposes of the solar industry, the FEOC rule prevents projects from claiming federal investment tax credits under sections 45Y and 48E if the project uses too many components from a Prohibited Foreign Entity or has certain ties to a PFE. It also prevents US manufacturers that use too many components from a PFE from benefitting from section 45X credits.

Chinese-made products are most likely to affect the solar industry. Other prohibited entities are Russia, North Korea, and Iran.

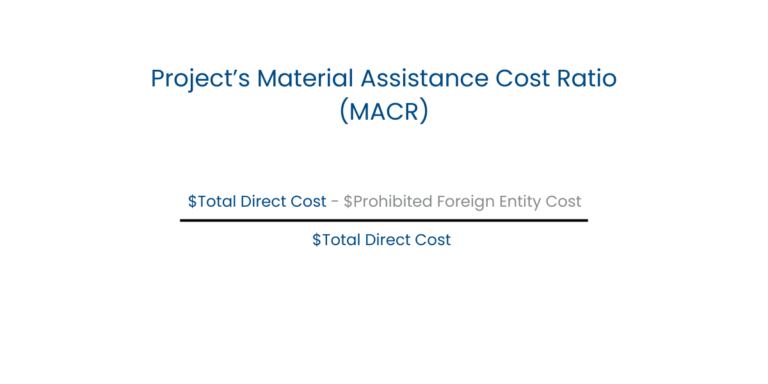

The calculation for “too many” components is below. The required Material Assistance Cost Ratio (MACR), which is the percentage of non-FEOC labor and materials used, varies by credit and technology. Refer to the IRS notice for specifics.

Who do the new FEOC rules apply to?

Solar developers or manufacturers that are identified to be foreign entities or foreign-influenced entities will be ineligible for tax credits, even if their products are sourced from non-FEOC countries. This includes companies that are at least 25 percent owned by a prohibited foreign entity. It also includes companies that grant effective control to a prohibited foreign entity.

Companies that operate under Chinese technology licenses or that have Chinese investments may now also be in violation of FEOC rules. If IP licenses grant effective control, they are not eligible for US clean energy tax credits. Companies with Chinese shareholders or debt held by Chinese lenders may also be ineligible. 2

Are the OBBBA’s FEOC rules already in effect?

The OBBBA established the start date for FEOC enforcement as “tax years beginning after July 4, 2025.” In other words, for calendar-year taxpayers, January 1, 2026.

Projects that established a beginning construction date before December 31, 2025 were safe harbored and do not need to meet the new FEOC requirements to qualify for clean energy tax credits.

Projects with a beginning construction date AFTER December 31, 2025 that don’t meet the FEOC rules will not be eligible for 45Y, 45X, or 48E tax credits.

Has the Treasury issued FEOC guidelines?

Draft guidance from the US Treasury department was released February 12. The draft confirmed that solar developers can use the cost percentages in the published domestic content safe harbor tables (IRS Notice 2025-08) until new safe harbor tables are released. New tables are expected by the end of the year. Taxpayers may also use supplier certifications to determine a project’s MACR. In either case, maintaining documentation is crucial.

Supplier certifications must be:

- Signed under penalty of perjury

- Include EIN/foreign tax ID

- Cover chain of production

- Address PFE sourcing or cost math

- Be retained for 6 years

There is still uncertainty around the definitions of “prohibited foreign entities” and “effective control,” though the February 12 release does explain that effective control includes intellectual property licensing agreements Note that after the Inflation Reduction Act was passed in 2022, it took about 20 months for final 30D FEOC guidance to be released.

What are developers and manufacturers doing to comply with FEOC?

According to a survey by tech company Crux, most clean energy developers and manufacturers are already taking steps to ensure FEOC compliance. This includes auditing contracts, mapping supply chains, and reviewing ownership. Still, the same survey found only about a third of companies feel “fully prepared” for 2026. 3

What happens if a taxpayer claims a clean energy tax credit but is not FEOC-compliant?

There are substantial financial penalties for taxpayers and corporations that violate the FEOC restrictions and claim clean energy tax credits. The IRS will have six years after a return is filed to challenge whether a project benefitted from material assistance from a specified foreign entity.

Additionally, if the taxpayer makes payments under disqualifying agreements any time in the following 10 years, the full tax credit amount must be repaid.

How to ensure solar projects are FEOC compliant?

It may be tricky to identify interactions with foreign entities or foreign-influenced entities that would put a project or company in violation of FEOC regulations. As always, consult an attorney or tax adviser.

When sourcing materials or project equipment, ensure you have identified their level of FEOC compliance. Sourcing domestically manufactured content from American companies is generally the safest way to ensure full FEOC compliance.

Kinect Solar has solar equipment that complies with all FEOC standards, in stock and ready to ship. Additionally, we are an Austin, Texas-based company without ties to specified foreign entities. Our solar experts can assist with procurement and project strategies to maintain FEOC compliance and maximize available clean energy tax credits*.

Sources and recommended reading

- https://www.projectfinance.law/publications/2025/july/working-through-the-feoc-maze/

- https://www.solarpowerworldonline.com/2025/12/feoc-rules-could-change-solar-panel-brand-trends-in-united-states/

- https://www.solarpowerworldonline.com/2025/12/feoc-rules-could-change-solar-panel-brand-trends-in-united-states/

* Kinect Solar makes no representations, warranties or guarantees regarding tax credit eligibility by any customer purchasing our products, any end user or successor in interest to the Products, or any property, project, system or facility claiming such credits, nor does it provide tax, legal, or accounting advice. Customers are strongly advised to consult your own tax, legal and accounting advisors regarding eligibility of your property, projects, systems or facilities for tax credits under Sections 45Y, 48E or any other provision of the Code.